The 28-Day Gap

I was watching the markets celebrate when the clause caught my eye.

February 2, 2026. Trump had just announced the India-US trade deal on Truth Social. Tariffs slashed from 50% to 18%. Markets up. Rupee strengthening. Every headline focused on the tariff number. But buried in the announcement was a single commitment that the Indian government never publicly confirmed: Modi had agreed to stop buying Russian oil.

I read it twice. Russian crude had been India’s discount lifeline for three years, sometimes running $15-20 below benchmark per barrel. More than that, Russian oil arrives via the Baltic and Black Sea, crosses the Suez or rounds the Cape. It never touches the Strait of Hormuz. I flagged it, kept scrolling through the trade deal coverage. Come back to Russia later.

Twenty-eight days after that deal, the Strait of Hormuz went dark. And the impact of that closure on India turned out to be far worse than anyone reporting on oil prices was willing to calculate.

Some context. India is the world’s third-largest oil consumer. It imports 88% of its crude to feed a domestic refining capacity that processes 5.6 million barrels every single day. The country produces a fraction of that domestically.

The question that matters is where that oil travels through.

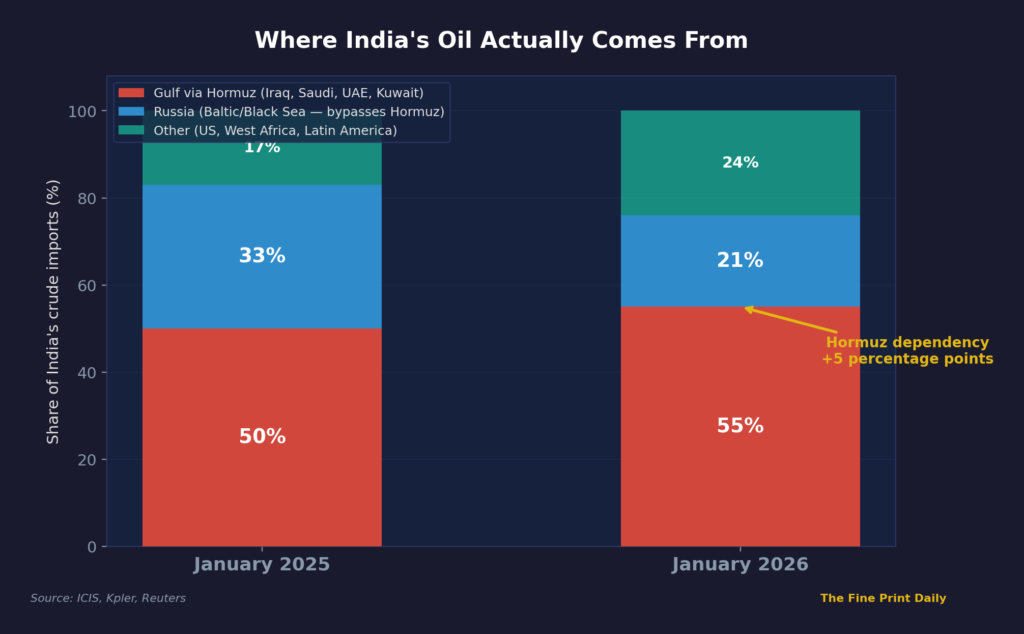

As of January 2026, the Middle East accounted for 55% of India’s crude imports, roughly 2.74 million barrels per day. That figure comes from ICIS, the commodities research group. Ajay Parmar, ICIS’s director of energy and refining, told Reuters that China has at least six months’ worth of crude in storage while Indian inventories are much lower.

55%.

More than half of India’s crude oil, travelling through a 33-kilometre gap between Iran and Oman. And in the first weeks of 2026, India had quietly increased its dependency on that gap by five percentage points.

How did India maximise its Strait of Hormuz exposure?

The answer traces back to the clause I flagged on February 2.

Throughout 2024 and into 2025, India had built a genuine hedge against Middle Eastern volatility. Russian crude, available at steep discounts after Western sanctions, had grown to 40% of India’s import basket at its peak. More than 2 million barrels a day, some months. India was buying oil that never needed to transit any chokepoint in the Persian Gulf.

Then came the tariffs. In August 2025, the Trump administration slapped a 25% punitive tariff on Indian exports specifically because of Russian oil purchases, on top of the existing 25% reciprocal tariff. 50% combined. Indian markets got hammered, the worst performer among emerging economies for 2025, with record outflows of foreign capital.

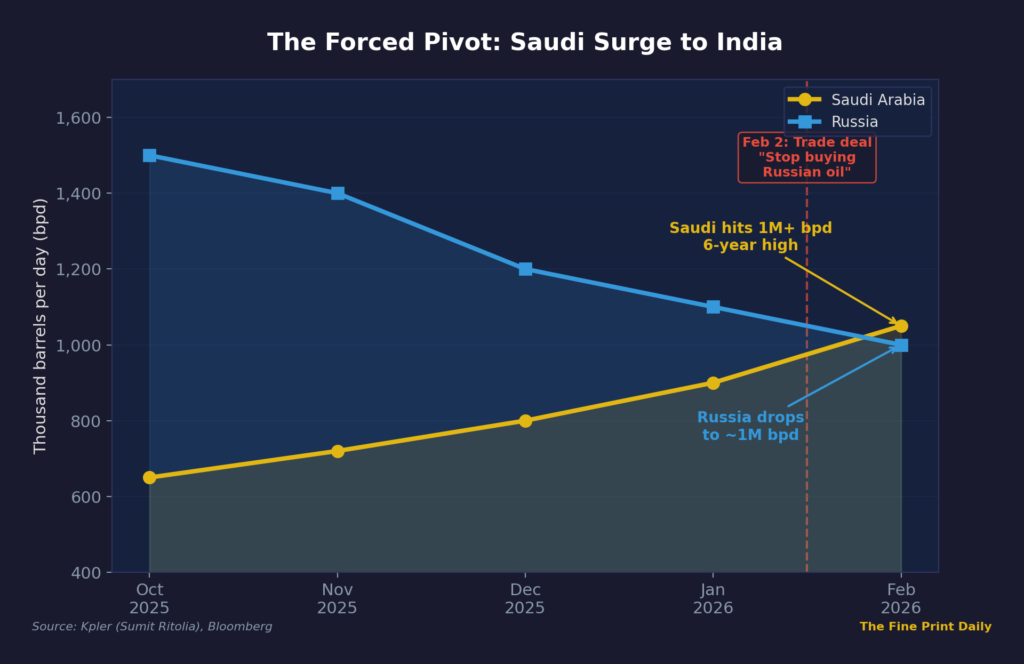

By January 2026, Russian crude’s share of India’s basket had fallen to roughly 21%, a 39-month low by Kpler’s volume tracking. Reliance Industries publicly stated it expected no Russian crude deliveries. To backfill those missing barrels, Indian refiners pivoted to the one place that could supply the volume at short notice: the Persian Gulf.

Saudi imports surged 30% month-on-month in February, crossing 1 million barrels per day for the first time in six years. Every single one of those Saudi barrels exits the Persian Gulf through the Strait of Hormuz.

I did the arithmetic. India gave up its one major supply route that bypasses Hormuz entirely, then replaced it with barrels that transit Hormuz exclusively. Net effect: Hormuz dependency jumped from around 50% to 55% in the space of a few months. India didn’t just lose a safety valve. It actively increased its exposure to the most dangerous chokepoint in global energy, weeks before that chokepoint closed.

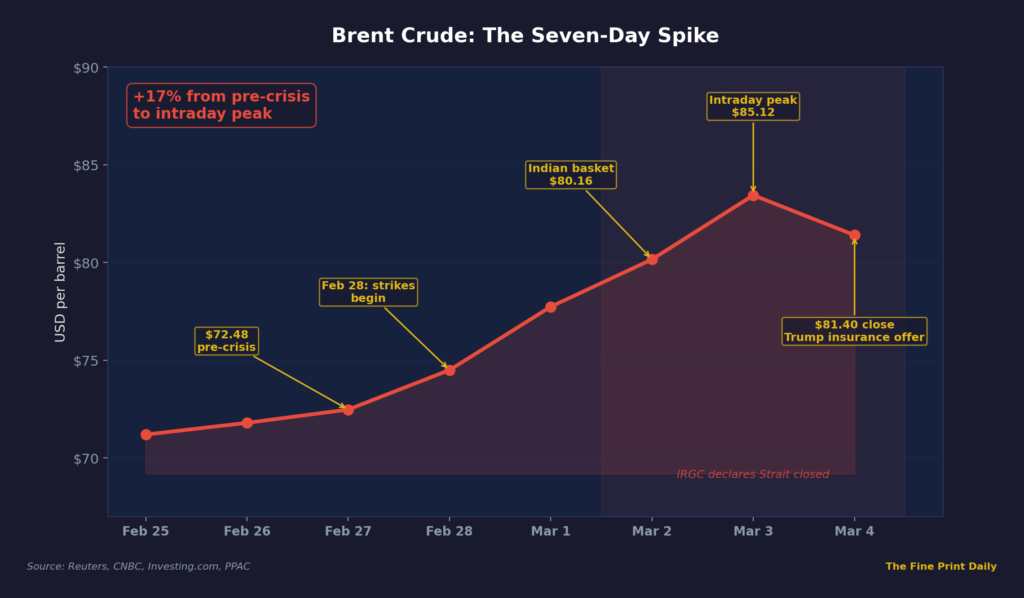

February 28. The United States and Israel launched coordinated strikes on Iranian nuclear and missile infrastructure. Operation Epic Fury. Supreme Leader Khamenei was killed. Iran retaliated with ballistic missiles on US and allied bases across the Gulf.

By March 1, the IRGC was targeting commercial shipping. The Marshall Islands-flagged tanker MKD VYOM was struck by an Iranian drone boat in the Gulf of Oman, breaching the hull above the waterline. Fire in the engine room. One Indian crew member killed. The US-flagged Stena Imperative was hit by projectiles while docked in Bahrain, killing a shipyard worker.

March 2. IRGC commanders declared the Strait of Hormuz closed to international navigation. Ebrahim Jabari, senior adviser to the IRGC commander-in-chief, said anyone attempting to pass would be set ablaze.

crude oil price surge from 72 to 85 dollars per barrel during Strait of Hormuz closure crisis March 2026

Kpler’s vessel tracking showed the collapse in real time. Transit volumes fell from 17-19 million barrels per day to roughly 2 million, almost entirely dark-fleet vessels. Maersk, MSC, Hapag-Lloyd, Japanese and Taiwanese carriers all suspended Persian Gulf operations.

But here’s what most coverage missed. The military threat didn’t close the strait on its own. The insurance industry did.

Major maritime insurance mutuals withdrew war-risk coverage for the Persian Gulf, effective March 5, 2026. Without indemnity insurance, moving a $120 million VLCC through an active war zone is mathematically impossible for any shipowner. The premium alone adds $600,000 or more per transit at wartime rates. The liability of a total hull loss makes the freight margin irrelevant. Ships don’t sail uninsured.

Kotak Securities called it a transit shock, not a price shock. They were right.

Does India have enough oil reserves for a Hormuz closure?

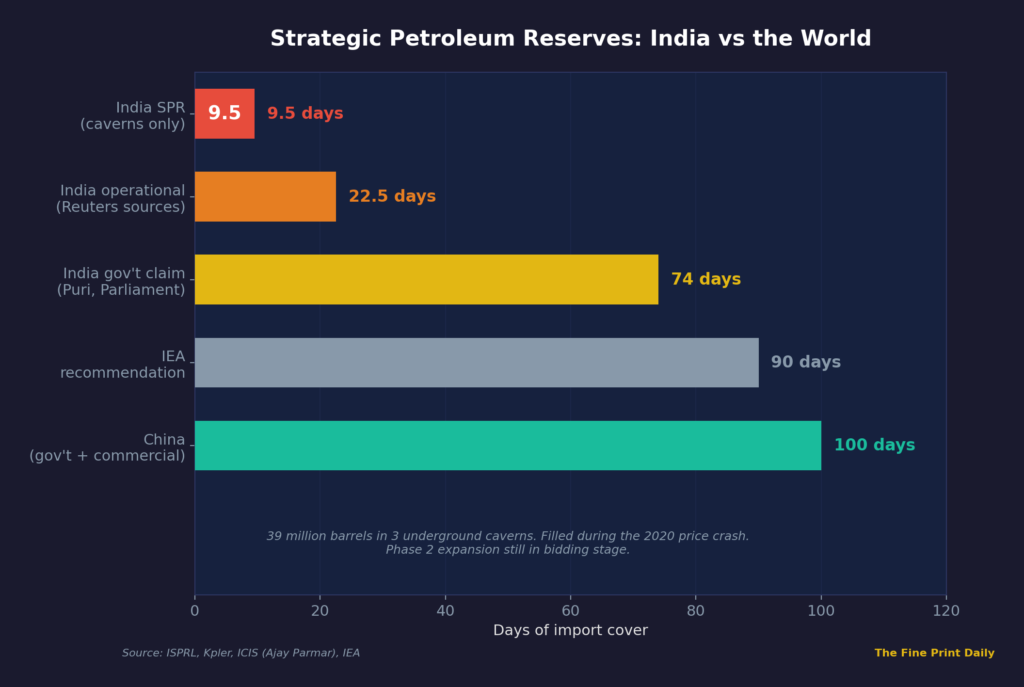

On February 9, three weeks before the strikes, Petroleum Minister Hardeep Singh Puri stood in the Rajya Sabha and told Parliament that India’s reserves could sustain the country for 74 days. His words, reported verbatim by Business Standard: together, if you look at the reserves in our caverns and what is held by our refineries and our floating platforms at our ports and our products, it comes to 74 days.

Comfortable number. Reassuring.

Then I pulled the Reuters factbox from March 2. Refining sources told Reuters that India’s current crude and refined fuel inventory could last for about 20 to 25 days.

74 days versus 20 to 25.

The discrepancy isn’t deception, it’s methodology. Puri’s 74-day figure is a theoretical maximum. It aggregates 9.5 days of dedicated Strategic Petroleum Reserves with 64.5 days of “commercial inventory,” which includes pipeline fill, tank bottoms, refined products in transit, crude sitting on floating platforms. Pipeline fill is oil required to keep the domestic distribution network pressurised and functional. You can’t extract it and refine it without shutting down the infrastructure it’s flowing through.

Refiners count differently. They tally only unencumbered liquid crude that can actually feed a distillation unit right now. By that metric, Kpler estimates India holds roughly 100 million barrels of usable commercial crude. Against daily consumption of 5.5 million barrels, that’s under 20 days of total coverage.

compared to China 100 plus days and IEA recommended 90 days of import cover

Nine and a half days.

That’s what India’s dedicated strategic reserves cover. Three underground rock caverns at Visakhapatnam, Mangalore, and Padur, holding 5.33 million metric tonnes, roughly 39 million barrels. China, for comparison, has built a stockpiling architecture totalling an estimated 1.2 billion barrels, over 100 days of pure import cover. India’s Phase 2 expansion, planned for Chandikhol and Padur, remains in the bidding stage. Zero physical relief for 2026.

I’d been doing what everyone else was doing. Tracking crude prices, counting reserve days, mapping tanker routes. Then I found the LPG data, and the investigation changed direction.

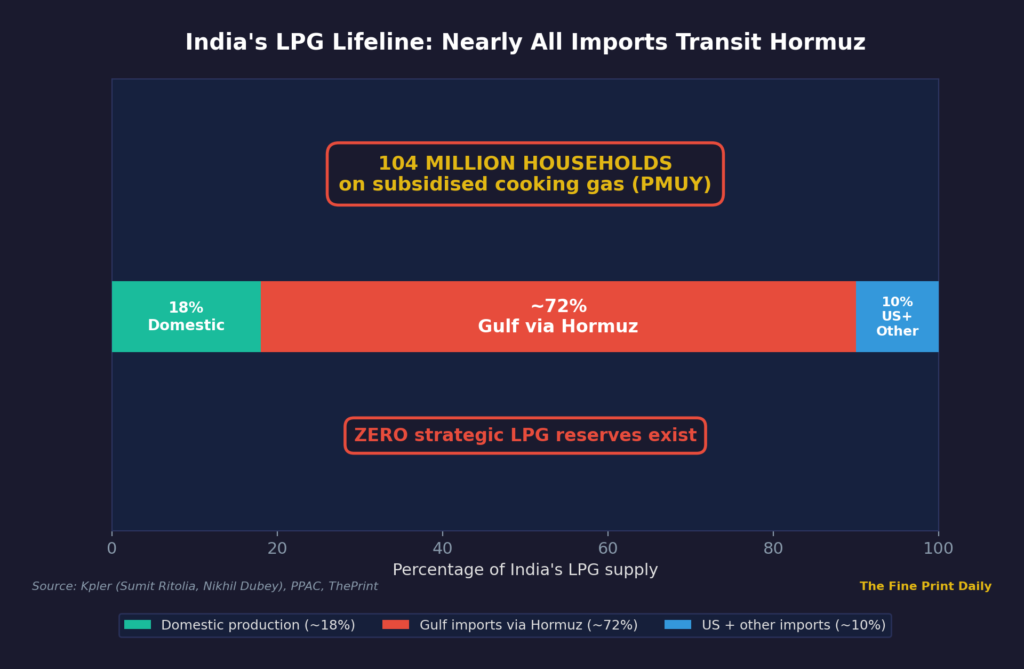

India imports 80 to 85% of its liquefied petroleum gas. That figure comes from Kpler’s lead research analyst Sumit Ritolia, confirmed independently by Nomura. And here’s the number that stopped me: nearly all of that imported LPG originates from Gulf suppliers and transits the Strait of Hormuz.

For crude oil, 55% transits Hormuz. For LNG, about 60%. For LPG, it’s close to 100%.

And unlike crude oil, India maintains no strategic LPG reserves. None. The specialised gas carriers required to transport LPG can’t be easily rerouted or replaced, and spot availability is thin. Kpler’s Nikhil Dubey put it directly: India imports almost all of its LPG through the Strait of Hormuz, and any disruption would immediately pressure flows.

I pulled the Ujjwala data. As of January 2026, over 10.4 crore connections are active under the Pradhan Mantri Ujjwala Yojana. That’s 104 million of India’s poorest households relying on government-subsidised LPG cylinders for cooking. The subsidy exists because the state absorbs the gap between international LPG prices and what these families can afford, through the oil marketing companies: IOC, BPCL, HPCL.

Those same OMCs carried an aggregate LPG under-recovery burden of Rs 41,270 crore into the previous fiscal year. Every $10 per barrel increase in crude, which drags petroleum gas prices with it, adds $13 to $14 billion to India’s annual import bill. The Indian crude basket has already jumped from $62 to $80 since December.

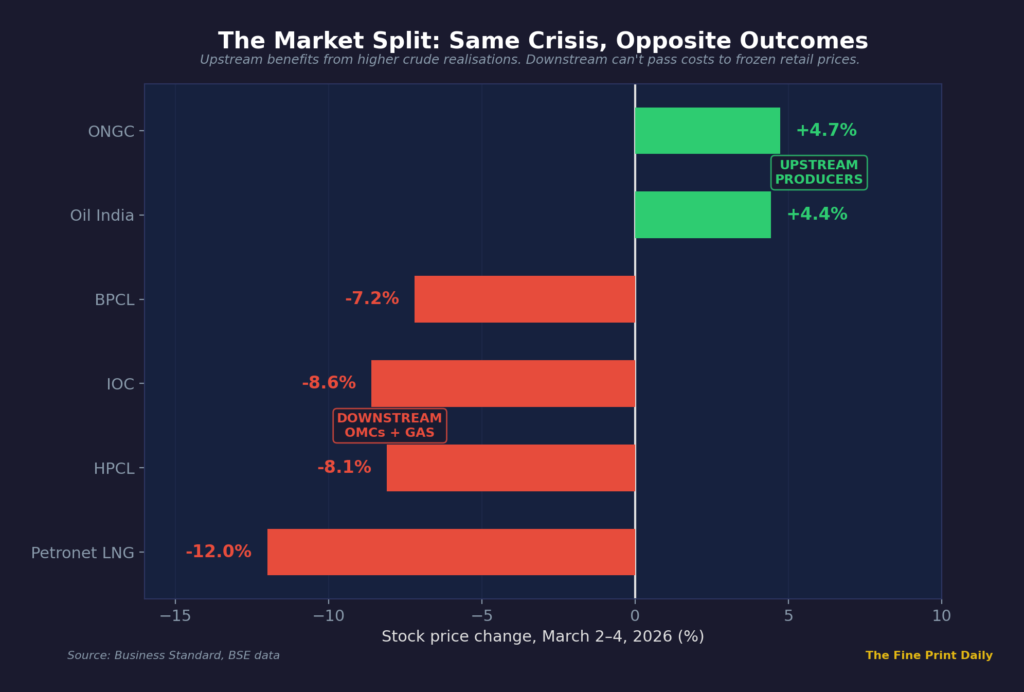

The market knew before the government spoke. In two trading sessions after the crisis began, BPCL fell 7.2%. IOC fell 8.6%. HPCL fell 8.1%. Petronet LNG crashed nearly 12% after QatarEnergy declared force majeure on its 77-million-tonne Ras Laffan facility following drone strikes, forcing Petronet to issue corresponding force majeure notices to its downstream customers: GAIL, IOC, BPCL.

And upstream? ONGC surged 4.73%. Oil India gained 4.43%. Higher crude means higher realisations on domestic production. Same crisis, opposite outcomes. The split between producers and marketers tells you exactly who absorbs the shock and who profits from it.

What India’s Strait of Hormuz crisis really means

‘d been asking the wrong question. I spent days tracking crude oil prices and tanker movements and Brent futures.

The right question was never about crude. Crude oil has alternatives. Russian barrels via the Arctic. West African spot cargoes. US shipments. Longer transit times, higher freight costs, but the barrels exist. India can source crude from outside the Gulf. It’s expensive, it’s slow, but it’s physically possible.

LPG has no alternative at the volume India needs, on the timeline that matters.

If the Strait of Hormuz stays closed for more than a few weeks, India doesn’t run out of petrol first. It runs out of cooking gas. And the 104 million families who depend on Ujjwala subsidies don’t have a backup plan. They don’t have a hedge. They have a government promise and a supply chain that runs through a war zone.

I closed the laptop around 3 AM, but the timeline kept running in my head. February 2: India agrees to give up Russian crude, its one supply route that completely bypasses Hormuz. February 20: Saudi shipments hit a six-year high, all transiting Hormuz. February 28: the Strait closes. March 5: insurance coverage cancelled.

Twenty-eight days from concession to crisis. And the concession is already fraying. Reports are surfacing that Indian officials are quietly discussing a rapid return to Russian Urals-grade crude as the primary relief valve. The trade deal is less than a month old and already under pressure.

I don’t know yet whether India reverses the Russian oil commitment. I don’t know whether the Strait reopens in days or weeks or months. But I know this: the gap between what the government told Parliament and what the refiners told Reuters is 49 days wide. And somewhere inside that gap, 104 million kitchens are counting down.