I was checking the Kpler data for early March when I noticed the number that should have raised eyebrows everywhere.

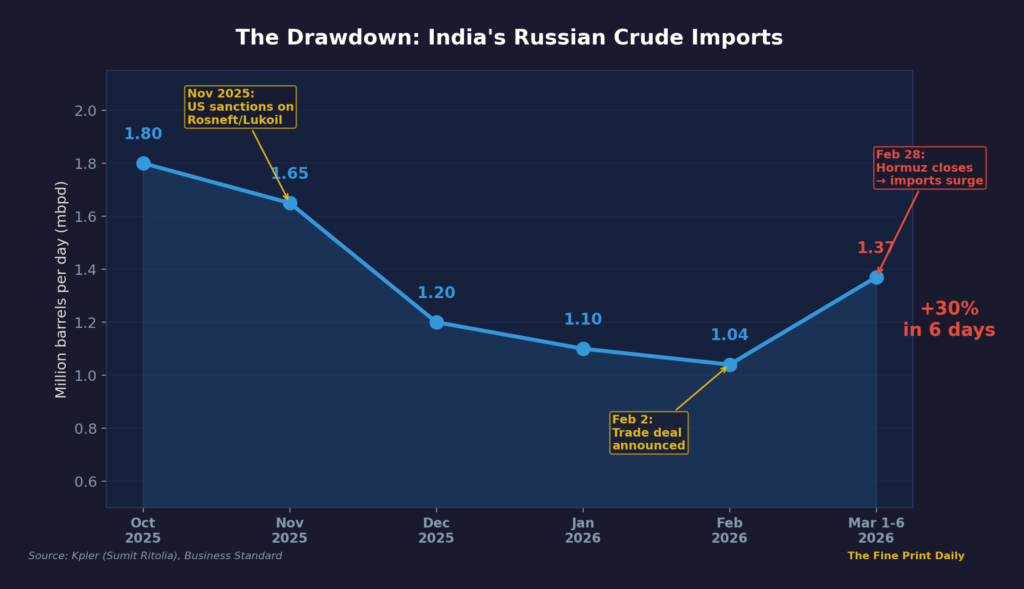

The India Russian oil waiver is bigger than it looks. India’s Russian crude imports for the first six days of March: 1.37 million barrels per day. That’s 30% higher than February’s 1.04 million. In a month where India had supposedly committed, under the terms of a trade deal signed barely five weeks earlier, to stop buying Russian oil entirely.

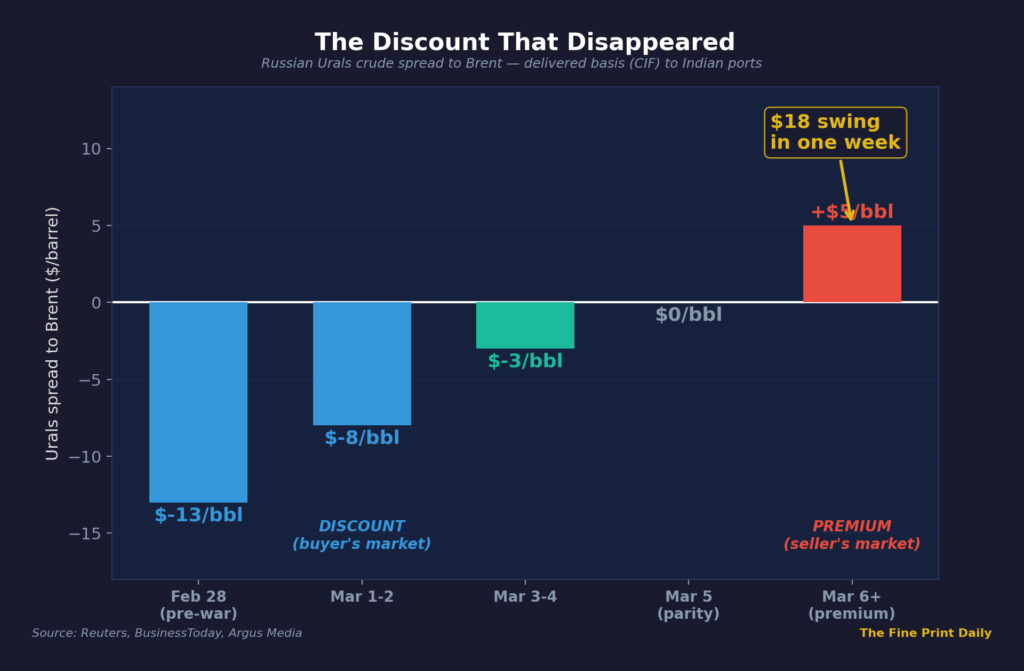

I pulled the pricing data next, and the second anomaly appeared. Russian Urals crude, the grade that had traded at a $13-per-barrel discount to Brent as recently as February 28, was now being offered to the same Indian refiners at a $4 to $5 premium. An $18 swing in under a week.

I’d spent Part 1 of this investigation tracing the 28-day gap between India voluntarily giving up its Hormuz bypass and the Strait shutting down. Now I was looking at something stranger: a trade deal that collapsed faster than the ink dried, a sanctions architecture that reversed itself, and a pricing inversion that shouldn’t exist in any textbook model of commodity markets.

Thirty-three days. That’s all it took from deal to reversal. And the reversal wasn’t just India’s. It was America’s.

Some history, because the speed of the collapse only makes sense if you understand what was being attempted.

On February 2, 2026, the Trump administration announced the India-US trade deal. The headline number was tariff relief: punitive duties on Indian exports slashed from 50% to 18%. Markets loved it. The Nifty 50 surged 2.5% the next trading day. The rupee gained nearly a percent.

Buried in the announcement, though, was what strategic analysts were already calling “the Russian oil clause.” According to the White House fact sheet, Modi had committed to stop buying Russian oil and pivot India’s procurement to American and other Western suppliers. The deal included a staggering $500 billion commitment to purchase American energy products, aircraft, precious metals, and coking coal over five years. An intent to purchase, technically. Not binding. But the implication was clear: tariff relief was the carrot, and Russian oil was the price.

India never confirmed the clause publicly. The joint statement omitted any mention of Russian oil. When pressed, the Ministry of External Affairs maintained what diplomats call “strategic ambiguity,” reiterating that India’s energy sourcing would be guided strictly by national interest. The Kremlin, for its part, said it had received no communication from India about any cessation.

But the data tells a different story from the diplomacy. Indian refiners did pull back.

How far did India actually cut Russian oil?

Key points: Oct ~1.80 → Nov ~1.65 → Dec ~1.20 → Jan ~1.10 → Feb 1.04 →first 6 days March 1.37

Source: Kpler (Sumit Ritolia), Business Standard

The drawdown was real. Kpler data shows Russian crude imports to India fell from roughly 1.8 million barrels per day in October 2025 to 1.04 million by February 2026, a 39-month low. The decline wasn’t driven solely by the trade deal. US sanctions on Rosneft and Lukoil, which took effect in late November 2025, physically constrained supply by cutting off refiners from direct liftings with Russia’s two largest producers.

The compliance had consequences. I traced this in Part 1: to backfill the missing Russian barrels, Indian refiners pivoted aggressively to the Persian Gulf. Saudi imports crossed 1 million barrels per day in February, a six-year high. Middle Eastern crude climbed to 55% of India’s total basket.

Every replacement barrel transited the Strait of Hormuz.

And then, on February 28, Operation Epic Fury began.

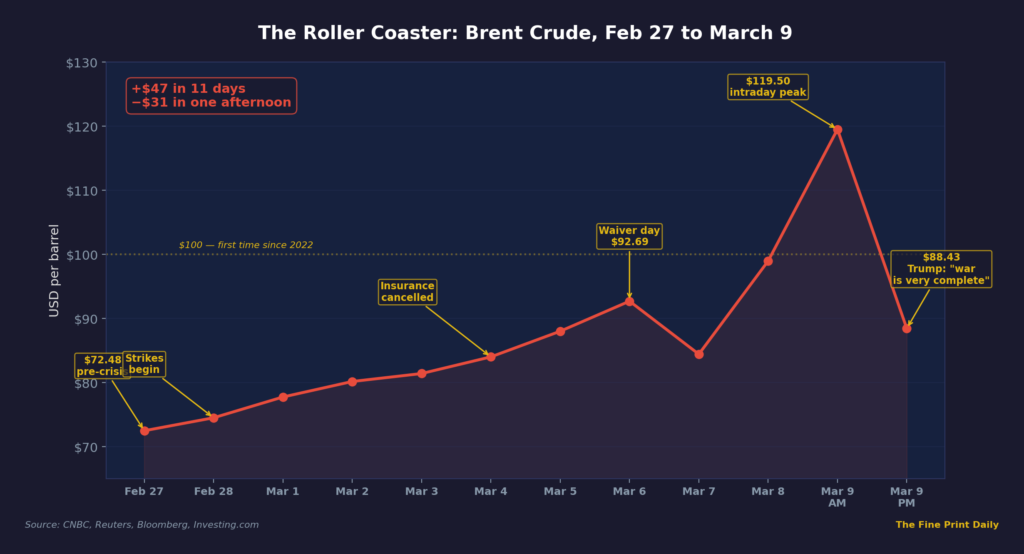

I covered the Strait’s closure in Part 1. What matters for this investigation is what happened to the data in the eleven days between February 28 and March 9. Because in those eleven days, the entire architecture of the India-US trade deal was demolished by arithmetic. Brent crude: $72 on February 27. By March 6, the day of the waiver, it had reached $92.69. By March 9, Brent hit an intraday peak of $119.50, the highest since Russia’s invasion of Ukraine. Then it crashed to $88.43 after hours when Trump told CBS News the war was “very complete, pretty much.” The oil market moved $47 in eleven days, then gave back $31 in a single afternoon.

Source: CNBC, Reuters, Bloomberg, Investing.com

Inside those price swings, something else was happening. Russia was repositioning its fleet.

Who moved first — India or Russia?

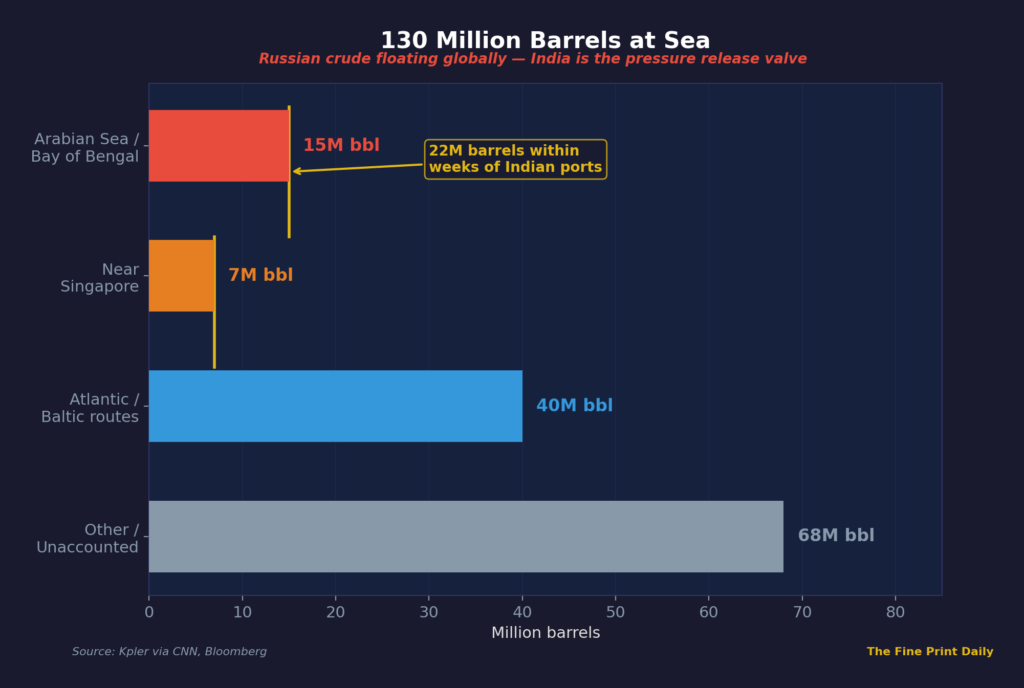

On March 4, four days before the US granted any waiver, Reuters reported that 9.5 million barrels of Russian crude were already sitting on tankers near Indian waters, ready for delivery within weeks. These cargoes had not originally been destined for India. They were floating stocks, stranded by sanctions and payment complications with Chinese buyers, now available to whoever needed them most urgently.

India needed them most urgently.

Indian state refiners — IOC, BPCL, HPCL, and MRPL — began aggressively approaching traders for prompt Russian cargoes. Bloomberg ship-tracking caught the rerouting in real time. The Suezmax Odune, carrying roughly 730,000 barrels of Urals crude, had been signaling an East Asian destination. Mid-ocean, it turned toward India and docked at Paradip. The Aframax Matari, loaded with another 700,000 barrels, executed the same manoeuvre toward Vadinar.

This was before the waiver. Indian refiners were buying Russian crude while the trade deal’s Russian oil clause was technically still in force.

The most telling signal came from Reliance Industries. India’s largest private refiner had deliberately scaled back Russian purchases from over 500,000 barrels per day to roughly 150,000 in the months before the crisis, complying with Western sanctions guidance to protect its European and American product exports. When the strait closed, Reliance reversed course within days, approaching traders to secure Russian cargoes and tapping floating oil from vessels anchored off India’s western coast. Keeping its massive Jamnagar refinery online superseded all previous regulatory caution.

The question everyone was asking — “Will India go back to Russian oil?” — was already the wrong question. India was already back. The waiver came after the fact.

What the waiver actually says

On March 5, OFAC issued General License 133. The legal structure tells you everything about how fast Washington was improvising.

The license authorises Indian entities to purchase Russian-origin crude and petroleum products loaded onto vessels on or before 12:01 AM EST on March 5, 2026. It expires at 12:01 AM EDT on April 4. Deliveries must occur at an Indian port, purchasers must be organised under Indian law. The license explicitly covers oil produced by sanctioned entities — Rosneft, Lukoil — and loaded onto blocked shadow fleet vessels.

Treasury Secretary Bessent framed it as pragmatism. “India is an essential partner,” he posted on X. “Our allies in India have been good actors.”

Source: White House, OFAC, CNBC, Moscow Times

Congressional Democrats didn’t see pragmatism. They saw capitulation. Representatives Liccardo and Gallego fired a letter to Bessent calling the waiver “dangerous, self-defeating, and indefensible,” pointing to intelligence reports that Russia was actively sharing targeting data against US military assets in the Middle East. “By providing this waiver,” they wrote, “you have signaled that the United States will reward attacks on our troops, not deter them.”

The administration’s defence was revealing. Energy Secretary Wright, appearing on CBS, called it a “pragmatic step” that diverts oil away from China. Bessent argued the waiver only applies to oil already stranded at sea, generating no new revenue for Russia.

The discount that disappeared

Here’s the detail that keeps me up at night. On February 28, hours before the first missiles hit Tehran, HPCL purchased two Aframax tankers of Russian crude at a discount of around $13 per barrel to Brent. Standard pricing for Urals in a sanctions-depressed market.

One week later, the same grade, offered to the same buyers, at a $4 to $5 premium over Brent. Delivered to the same Indian ports.

Source: Reuters, BusinessToday, traders

An $18 swing. In a week.

I need to be precise about what this means, because the mechanics matter. The premium is on a delivered basis — cost, insurance, and freight included. At the Russian wellhead, Urals was still trading at a deep FOB discount of around $30 to Brent. The Argus Media data from Primorsk showed $54.82 per barrel versus Brent at $82 on March 4.

The entire discount was eaten by logistics. Freight costs surged from $10-12 million per voyage to over $15 million. War-risk insurance premiums exploded. Tanker availability collapsed as vessels clustered outside the Gulf, refusing to transit. By the time Russian crude reached an Indian refinery gate, every dollar of the sanctions discount, the very discount that had made Russian oil attractive to India for three years, had been consumed by the crisis it was now being used to solve.

Russia didn’t raise its prices. The war did.

The ghosts in the strait

While India was securing Russian crude around Hormuz, a few operators were running through it.

Windward Maritime Intelligence tracked what might be the most audacious commercial transit of the crisis. A tanker carrying approximately one million barrels of crude, loaded at Saudi Arabia’s Juaymah Terminal, switched off its AIS transponder around March 4 and went dark. Five days later, the signal reappeared in the Gulf of Oman. A million barrels, navigated blind through an active war zone, presumably to capture freight premiums that made the risk mathematically rational.

Meanwhile, 55 Chinese-flagged ships remained trapped inside the Persian Gulf. CSIS data showed that despite Beijing’s deep diplomatic alignment with Tehran, only two Chinese vessels had transited the strait since March 1. The bulk carrier Iron Maiden tried a different approach: it exited the strait broadcasting “CHINA OWNER” on its AIS signal, betting that Chinese commercial identity would provide immunity.

It didn’t work at scale. Beijing’s diplomatic leverage, the same leverage that was supposed to guarantee Chinese energy flows in any Gulf crisis, bought exactly two transits in nine days

Source: CSIS, Windward, Kpler, Bloomberg

What India’s Russian oil waiver really means

I’d been asking the wrong question for the second time in this investigation.

Part 1, I asked “how high will oil prices go?” when the real question was about LPG and 104 million kitchens. This time, I asked “will India go back to Russian oil?” when the real question was: did India ever actually stop?

Kpler’s lead analyst Sumit Ritolia put it directly: the decline in volumes reflected “sanctions pressure, tariffs, payment issues, shipping constraints and evolving trading conditions rather than a deliberate policy pivot away from Russian barrels.” Russia remained India’s largest crude supplier throughout January and February 2026, even at the lowest import volumes. The drawdown was tactical compliance, not strategic realignment.

And New Delhi made this explicit. When the US framed GL 133 as a benevolent concession to an “essential partner,” India’s government responded with a statement that buried the trade deal’s Russian oil clause permanently: “India has never depended on permission from any country to buy Russian oil.”

The trade deal attempted something that the data always said was impossible. India imports 88% of its crude. It processes 5.5 million barrels a day. You cannot rearrange supply chains of that magnitude by diplomatic announcement, especially when the alternative suppliers all transit a single 33-kilometre chokepoint that any regional conflict can close.

The February 2 deal didn’t fail because of bad faith. It failed because the arithmetic was never workable. The Hormuz crisis didn’t break the deal. It revealed that the deal was never real.

I closed the laptop and pulled up the Kpler feed one more time. Eighteen tankers carrying Russian Urals crude were now showing India as their destination. The discount was gone, the premium was in, and the trade deal was 33 days old and already dead.

The question I still can’t answer: what happens on April 4, when GL 133 expires? Does Washington extend it, admitting the sanctions architecture is permanently compromised? Or does it let the waiver lapse, reimposing restrictions on an energy relationship that just proved itself indispensable?

I don’t know. But 130 million barrels of Russian crude are floating on the world’s oceans right now, and every refiner on the planet knows exactly where to find them.

Part 3: The Ghost Ships of Shandong