‘Europe Energy Crisis Hormuz 2026.’ I can see people typing this a few weeks from now as the gas prices surges.

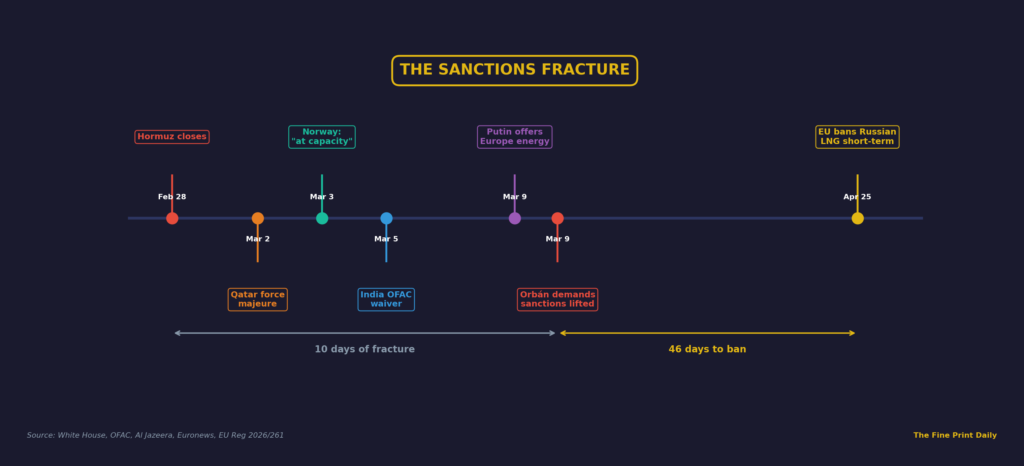

I was watching Putin’s televised address on March 9 when I realised he wasn’t talking to his oil executives. He was talking to Europe.

“We’re ready to work with Europeans too,” he said, flanked by the heads of Russia’s largest energy conglomerates. “But we need some signals from them that they’re ready and willing to work with us and will ensure this sustainability and stability.”

I wrote that down. Sustainability and stability. Those are contract terms, not diplomatic pleasantries. Putin was offering Europe a deal: dismantle the sanctions, and the gas flows resume. Keep the sanctions, and Russia redirects what’s left of its European LNG to Asia, where buyers are already paying premiums.

I’d spent Part 1 of this investigation tracing how India maximized its Hormuz exposure 28 days before the Strait closed. Part 2 followed the 33-day collapse of the India-US trade deal and the $18 swing in Russian crude pricing. Now I was looking at the same arithmetic playing out on a different continent, with higher stakes and less room to manoeuvre.

Europe’s problem isn’t oil. Europe can survive expensive oil. Europe’s problem is gas. And the numbers are worse than anyone on television is admitting.

How empty is Europe’s gas tank?

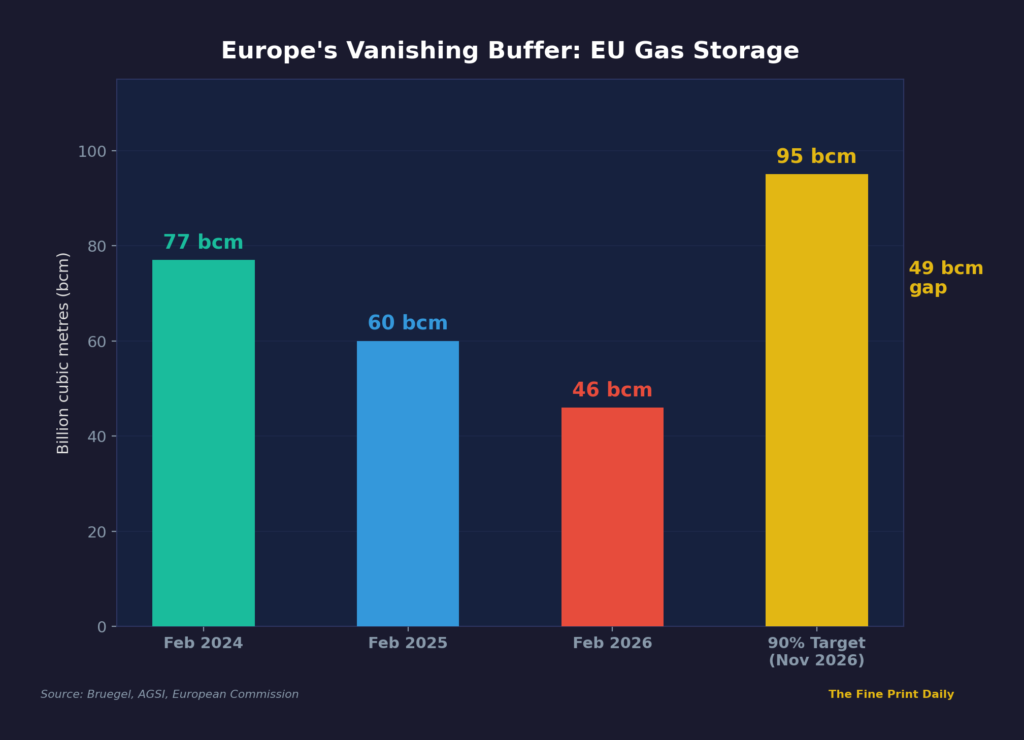

I pulled the Bruegel dataset. EU gas storage stood at 30% of capacity at the end of February 2026. That’s 46 billion cubic metres in the ground. For context: the same facilities held 60 bcm a year earlier, and 77 bcm the year before that.

Annotations: “46 bcm → needs to reach ~95 bcm by November. That’s 49 bcm of injection in 8 months.”

Source: Bruegel, AGSI, European Commission

The Netherlands, the hub where European gas actually trades, was at 10 to 20%. Germany and France below 30%.

The depletion wasn’t accidental. An unusually cold winter pushed gas demand up 7% year-on-year. Europe simultaneously increased piped gas exports to Ukraine by more than tenfold since the start of 2026, draining nearly 0.9 bcm from reserves to keep Ukraine’s grid alive after Russian transit ended.

And then on February 28, the Strait of Hormuz closed. And with it, Europe’s second-largest alternative to Russian gas disappeared overnight.

Here’s the arithmetic that nobody in Brussels wants to say out loud.

The EU’s Gas Storage Regulation requires member states to fill storage to 90% by the start of winter. Aggregate EU storage capacity is roughly 105 bcm. Ninety percent of that is about 95 bcm. Europe currently has 46 bcm. The injection gap is 49 bcm, minimum, and that’s before accounting for daily consumption that continues through spring and summer.

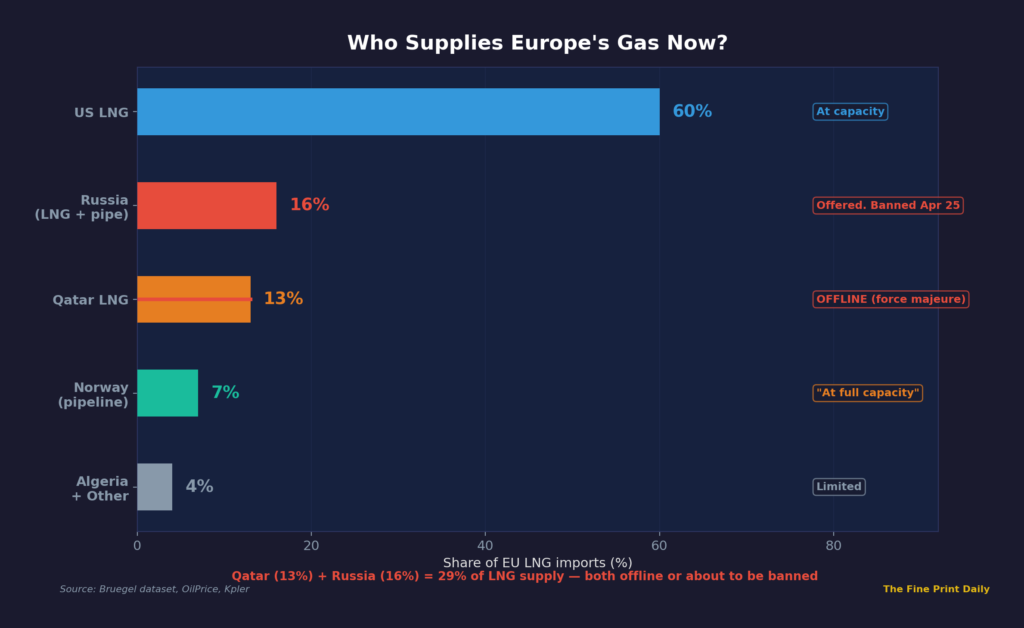

Kpler’s gas analysis team confirmed the scale of the supply hole. QatarEnergy’s force majeure on Ras Laffan removed 5.8 million tonnes of LNG from global supply in March alone, roughly 14% of the entire month’s expected global output. Qatar normally supplies 12 to 14% of Europe’s LNG imports. That baseline volume is gone.

The question is where replacement gas comes from.

Annotations: “Qatar offline. Russia offered. US at capacity. Norway: ‘We are producing at full capacity.'”

Source: Bruegel dataset, OilPrice

I checked Norway first. Norway’s Energy Minister Terje Aasland told Bloomberg on March 3: “We are essentially producing at full capacity. I don’t think there is much additional output to be found.” He added, quietly, that the crisis would likely reopen the debate on Russian gas.

The United States supplies 60% of Europe’s LNG. American terminals are already running near capacity. Kpler’s analysis was blunt: realistic supplementary LNG supply from all alternative global sources totals under 2 million tonnes against a 5.8-million-tonne monthly shortfall. The maths doesn’t close.

The price of panic

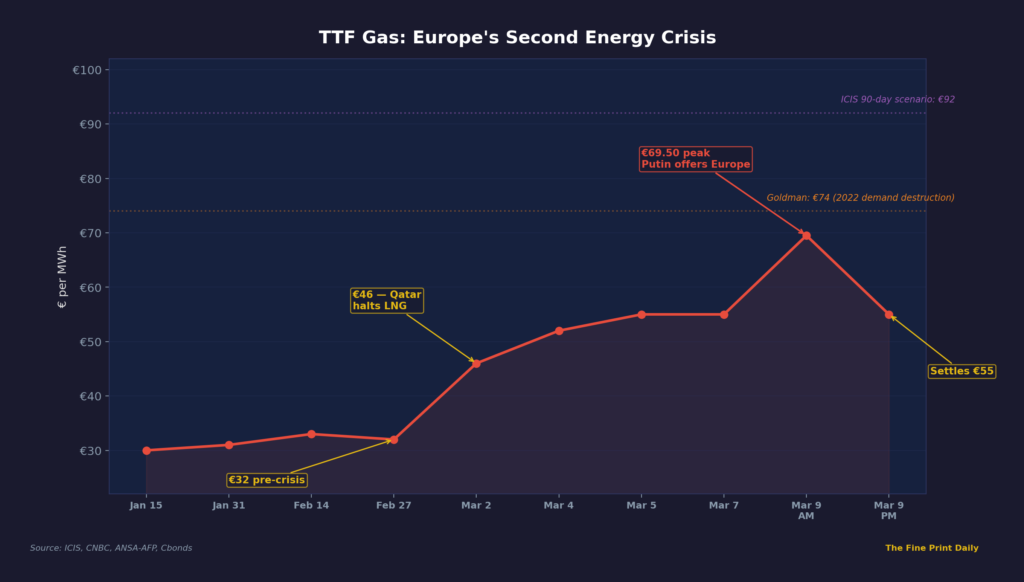

The gas market saw it before the politicians did.

Before the strikes, the Dutch TTF benchmark, the price that determines what European factories and households pay for gas, sat at around €32 per megawatt hour. By March 2, after the Hormuz closure and Qatar’s production halt, it had surged 45% to roughly €46. By March 9, TTF jumped another 30% to hit €69.50 intraday before settling around €55.

Key points: Feb avg ~€32 → Mar 2 ~€46 (Qatar halt) → Mar 7 ~€55 (50% weekly gain) → Mar 9 €69.50 intraday → settles ~€55

Annotations: “Feb 28: Strikes begin” / “Mar 2: Qatar halts LNG” / “Mar 7: Biggest weekly jump since 2023” / “Mar 9: €69.50 — Putin offers Europe energy”

Source: ICIS, CNBC, ANSA-AFP, Cbonds

ICIS ran the disaster scenario. Their head of energy analytics, Andreas Schroeder, modelled a 90-day Hormuz closure. The result: TTF immediately jumps to €92 per megawatt hour, averaging €86 across the blockade period. That’s nearly triple the pre-crisis level. At those prices, European heavy industry, chemical manufacturing, and fertiliser production become economically unviable. Germany faces mandatory gas curtailments. The 2022 energy crisis repeats, except this time storage starts lower and the conflict isn’t in Ukraine, it’s on the waterway that carries 20% of the world’s energy.

Goldman Sachs warned that a month-long halt would push TTF to €74, the exact level that triggered industrial demand destruction in 2022.

Serbia’s President Vučić said what the Western leaders wouldn’t: a prolonged closure means “hell in Europe.”

The impossible triangle

I started mapping the decisions on a whiteboard and hit the same structural problem three times.

Western governments are trying to do three things simultaneously. Enforce sanctions on Russia, the world’s second-largest energy exporter. Accept the Hormuz closure as a consequence of the military campaign against Iran. And keep their economies running, their factories lit, their households heated.

Pick any two. You cannot have all three.

India figured this out first. I traced it in Part 2: when the Strait closed, India broke the sanctions corner. It secured 20 million barrels of Russian crude via the OFAC waiver, paying a $4-5 premium over Brent for oil that had traded at a $13 discount just days earlier. India chose economic survival over sanctions compliance. Washington agreed, because the alternative was $150 oil.

Europe is now staring at the same triangle. And the cracks are already showing.

Annotations: “India broke Corner 1 (OFAC GL 133, March 5)” / “Europe is cracking at Corner 1 (Hungary, Slovakia, April 25 deadline)”

Source: Analytical framework

Who breaks first in Europe?

Hungary moved within hours of Putin’s offer. Foreign Minister Szijjártó demanded the EU immediately lift its ban on Russian oil and gas imports, arguing that maintaining “ideology” over supply reality would cause “serious harm to European people.” Prime Minister Orbán went directly to European Commission President von der Leyen with the same demand.

Slovakia escalated further. Prime Minister Fico filed a formal legal complaint against the European Commission’s decision to phase out Russian gas, calling it “ideology and hatred towards Russia” destroying his economy. On March 8, Fico threatened to coordinate with Hungary to veto a €90 billion EU loan package for Ukraine unless Russian energy flows are restored.

The institutional centre tried to hold the line. European Commissioner Dombrovskis insisted after an emergency Eurogroup meeting that Europe must “keep the pressure on Russia to prevent it from filling its war chest,” explicitly warning member states against panic-driven sanctions relief.

And here’s where the calendar turns into a weapon.

Source: composite

April 25, 2026. That’s when EU Regulation 2026/261 bans all Russian LNG imported under short-term contracts. Russia is currently Europe’s second-largest LNG supplier, accounting for 16% of total LNG imports as of February. The EU is about to legally prohibit purchases from a supplier it desperately needs, at the exact moment the global LNG market is 5.8 million tonnes short per month.

I sat with that number for a while. Sixteen percent. Qatar provided 12 to 14%. Qatar is offline. Russia provides 16%. Russia is about to be banned. That’s 28 to 30% of Europe’s LNG imports either gone or legally prohibited, simultaneously, with storage at 30% and winter eight months away.

The Atlantic Council argued forcefully for doubling down on sanctions, warning that if Europe backtracks, Moscow achieves “something more durable than short-term revenue gains: restored leverage.” They’re right about the geopolitics. But sanctions don’t generate molecules. And Europe needs roughly 49 billion cubic metres of molecules injected underground before November, or the continent enters the 2026-27 winter with storage levels that make the 2022 crisis look comfortable.

The bypass that doesn’t work

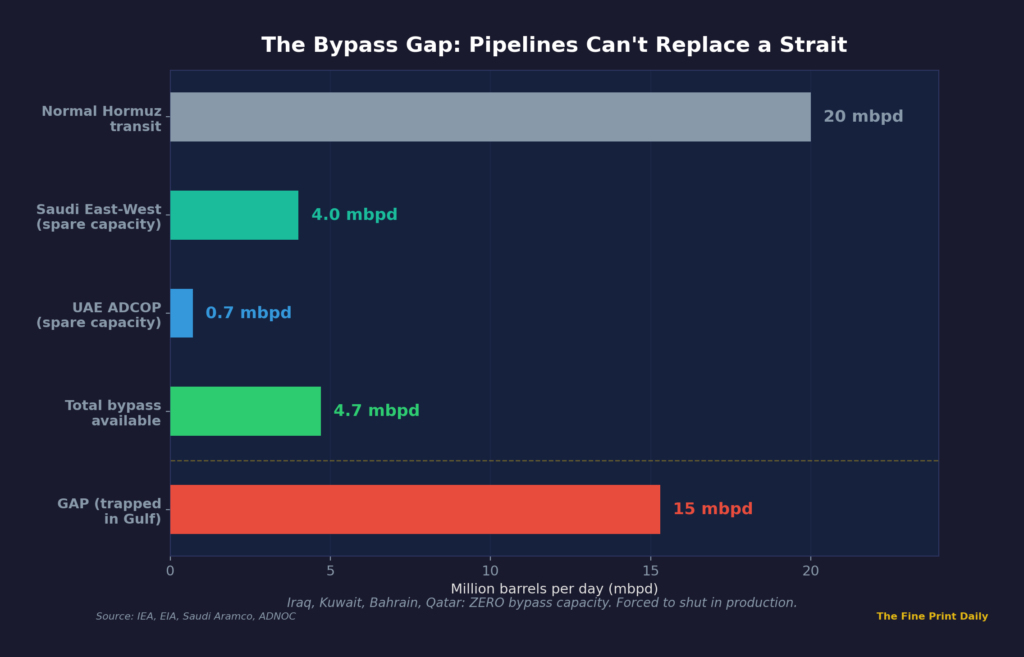

I checked the alternative everyone keeps mentioning. Saudi Arabia has the East-West Pipeline, which can move crude from the Persian Gulf coast to the Red Sea port of Yanbu, bypassing Hormuz entirely. The UAE has the Abu Dhabi Crude Oil Pipeline to Fujairah, outside the Strait.

Combined spare capacity: roughly 3.5 to 5.7 million barrels per day. The Strait normally carries 20 million. That leaves 14 to 16.5 million barrels per day physically trapped.

The bottleneck isn’t even the pipelines. It’s the ports. Yanbu’s loading terminals can sustain roughly 3 to 4 million barrels per day, but attempting to push 7 million barrels daily through two terminals designed for 4 creates massive offshore queues. Pakistan already sent an emergency request on March 4, formally asking Saudi Arabia to prioritise its oil shipments via Yanbu. Saudi Arabia has to decide which allied nation gets the limited loading slots and which nation waits.

Iraq, Kuwait, Bahrain, Qatar: no bypass pipelines at all. Those producers are shutting in production because their storage tanks are full and there’s nowhere for the oil to go.

Annotations: “Iraq, Kuwait, Qatar: zero bypass capacity. Forced to shut in production.”

Source: IEA, EIA, Aramco, ADNOC

What Europe’s energy gamble means for India

Here’s the thread that connects this back to where we started.

In Part 2, I documented India securing 20 million barrels from the 130 million barrels of Russian crude floating globally. India paid a $4-5 premium for oil that used to come at a $13 discount. Expensive, but it kept refineries running.

If Europe enters that same market, the premium gets worse for everyone.

The 130 million barrels aren’t a bottomless reservoir. Every barrel India takes is one Europe can’t. Every barrel Europe bids on drives the delivered price higher for India. Russia doesn’t need to choose a favourite buyer. Russia just needs both buyers competing, and the premium escalates on its own.

Euronews analyst Andrei Covatariu from the Energy Centre for Central Europe identified the deeper strategic play. Moscow could deliberately hold its crude discounts rather than cash in, he said, using the crisis “to deepen its leverage over Beijing” while India and Europe bid against each other for floating cargoes. Russia turns a crisis it didn’t start into a strategic asset.

Putin’s March 9 address made one thing explicit: he’s considering cutting off remaining European LNG deliveries entirely and redirecting them to Asia, pre-empting the EU’s own April 25 ban. If that happens, Europe loses Russian supply before it can replace it, and every LNG cargo in the Atlantic becomes the subject of a bidding war between European utilities and Asian refiners already desperate for gas.

The question I can’t answer

I’ve been running variations of the impossible triangle for ten days now, across three parts of this investigation. India’s version resolved quickly: break the sanctions corner, secure Russian crude, assert sovereignty. India’s response to the crisis was blunt, fast, and effective.

Europe’s version has no clean resolution. Break the sanctions corner, and Putin wins a historic diplomatic victory that funds the Ukraine war. Maintain sanctions through April 25, and Europe enters summer with 28-30% of its LNG supply legally or physically prohibited, storage at 30%, and a TTF price heading toward €90. Accept bypass infrastructure as sufficient, and the maths laughs at you: 5 million barrels per day doesn’t replace 20 million.

German Chancellor Merz stood at the White House on March 3 and said what every European leader is thinking but only one had the position to say publicly: “This is, of course, damaging our economies, this is true for the oil prices and this is true for the gas prices as well.”

That was seven days ago. Since then, oil has hit $119.50, TTF has touched €69.50, Qatar’s entire LNG output is offline, Russia has offered to fill the gap, Hungary and Slovakia are threatening to break the EU consensus, and the April 25 ban is 46 days away.

I don’t know what Europe chooses. I know the arithmetic. And the arithmetic says the impossible triangle resolves itself whether Brussels makes a decision or not.

Part 4 of The Oil Detective will examine how $100 oil reshapes the global economic outlook — from US midterm calculations to Federal Reserve rate decisions.